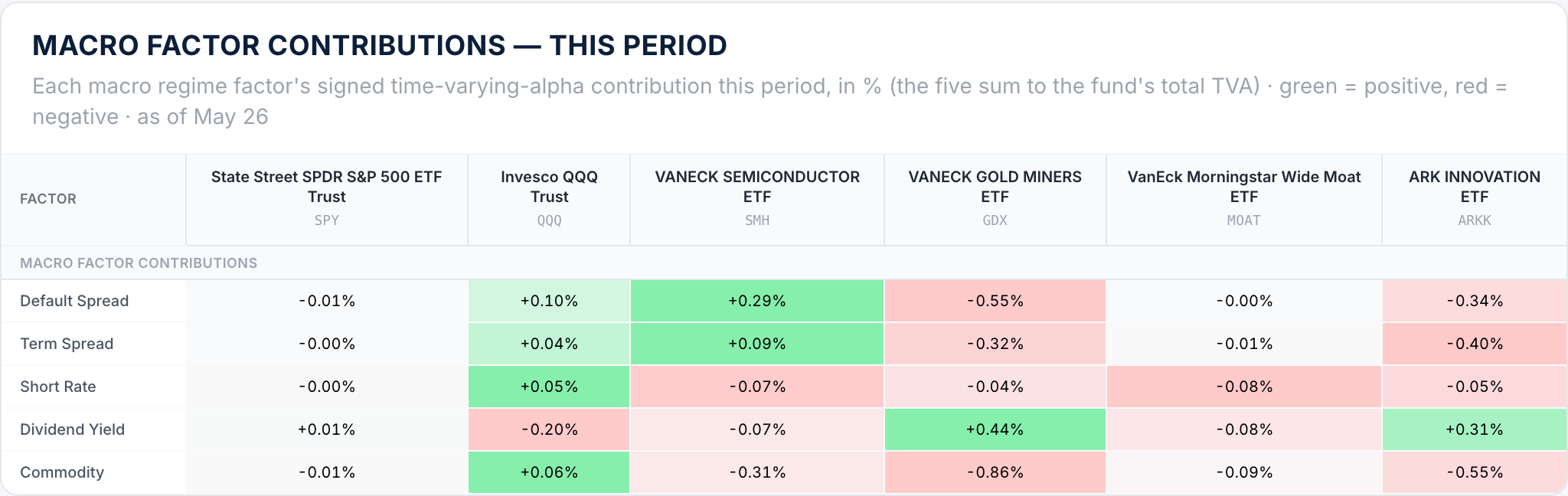

The macro engine

Alpha depends on the regime

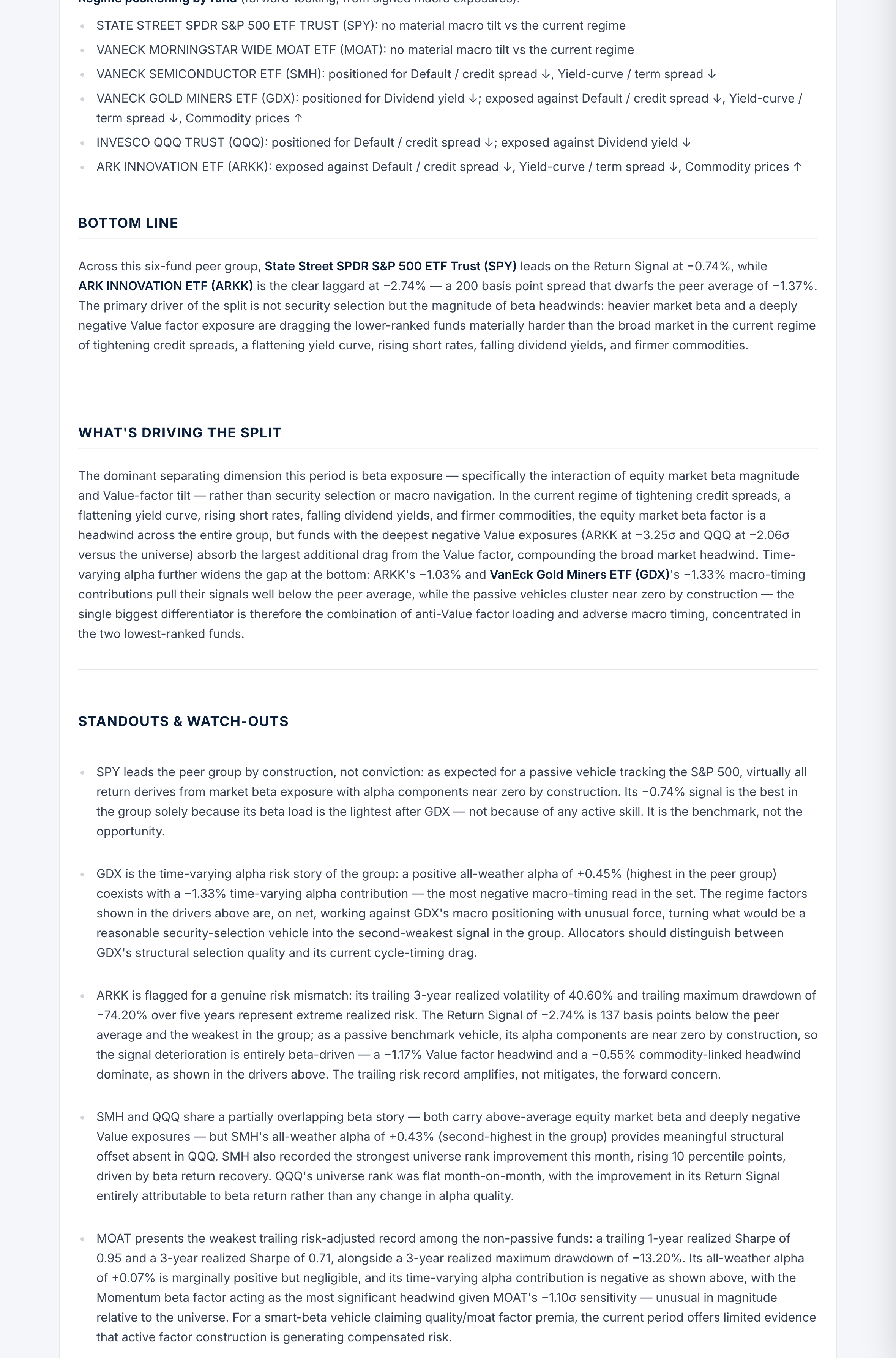

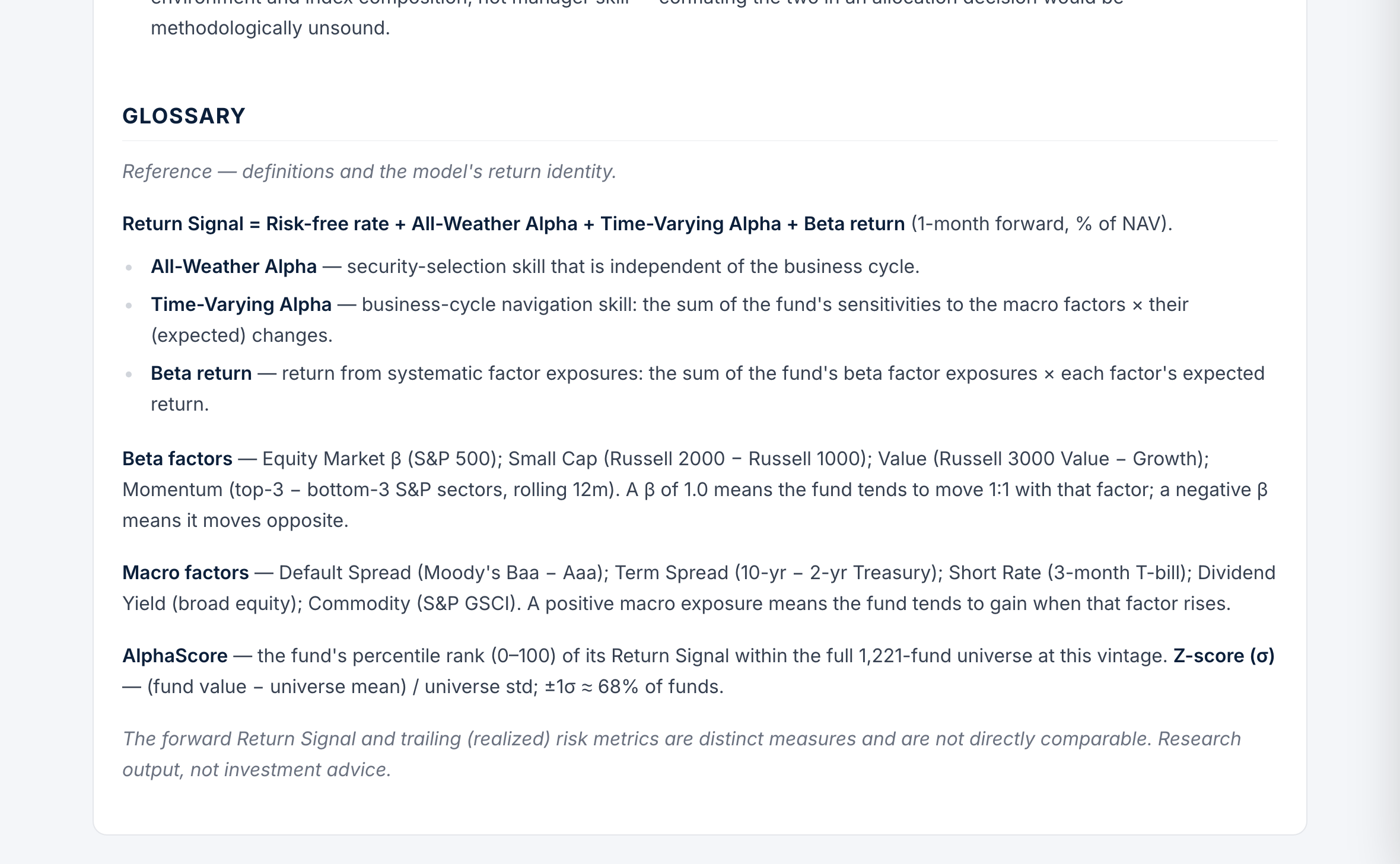

Most models estimate one static alpha per fund. AlphaPredictor® splits it in two: all-weather alpha, earned in any environment, and time-varying alpha — the part a fund earns in this macro environment, driven by its sensitivity to five regime factors: default spread, term spread, short rate, dividend yield and commodities.

Below, each fund's monthly Return Signal is split into the contribution from every regime factor — green where a factor added to the signal this month, red where it subtracted. The model re-estimates these as the regime shifts.

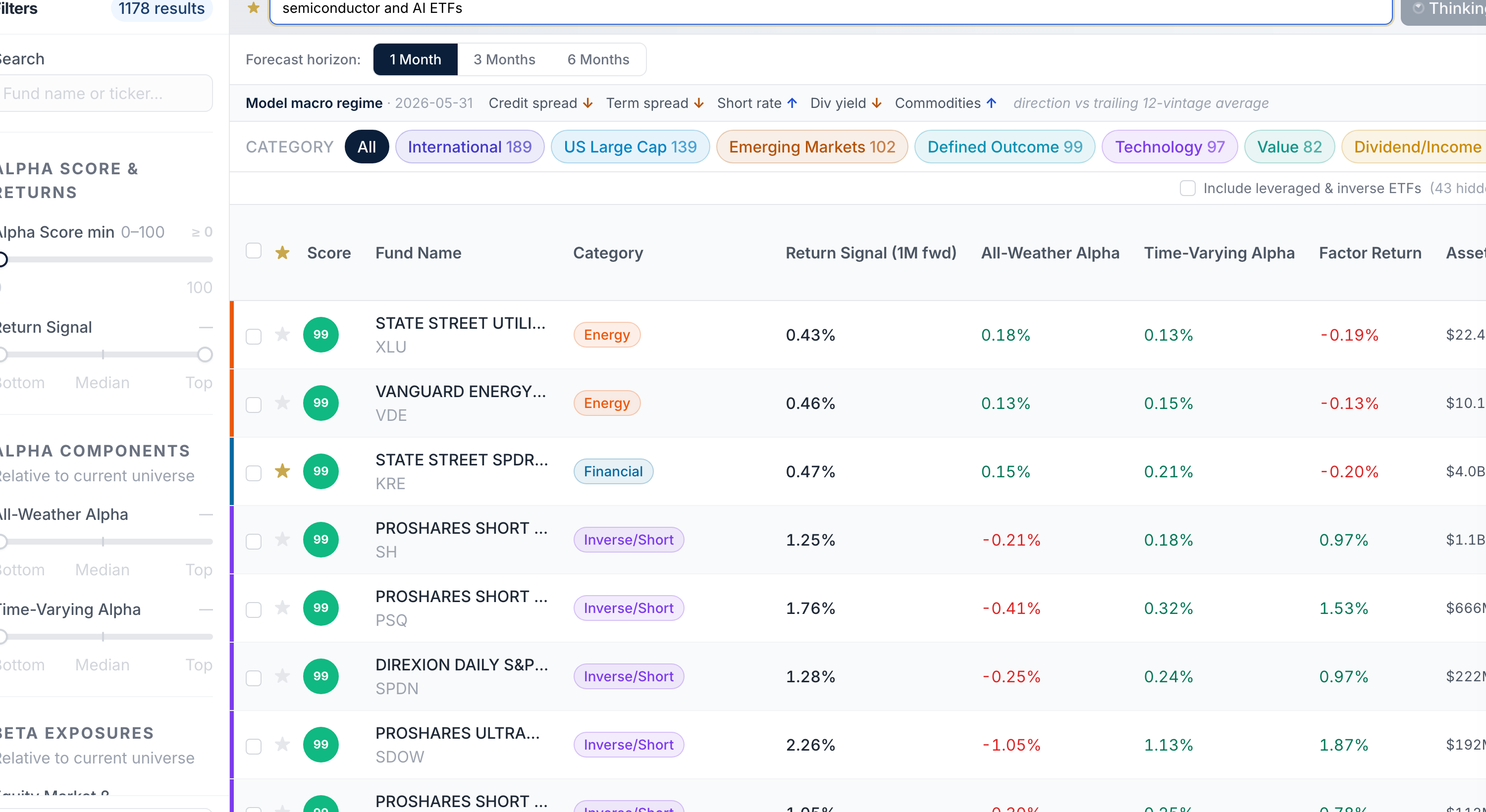

The AlphaScore™

A single, defensible number for every fund

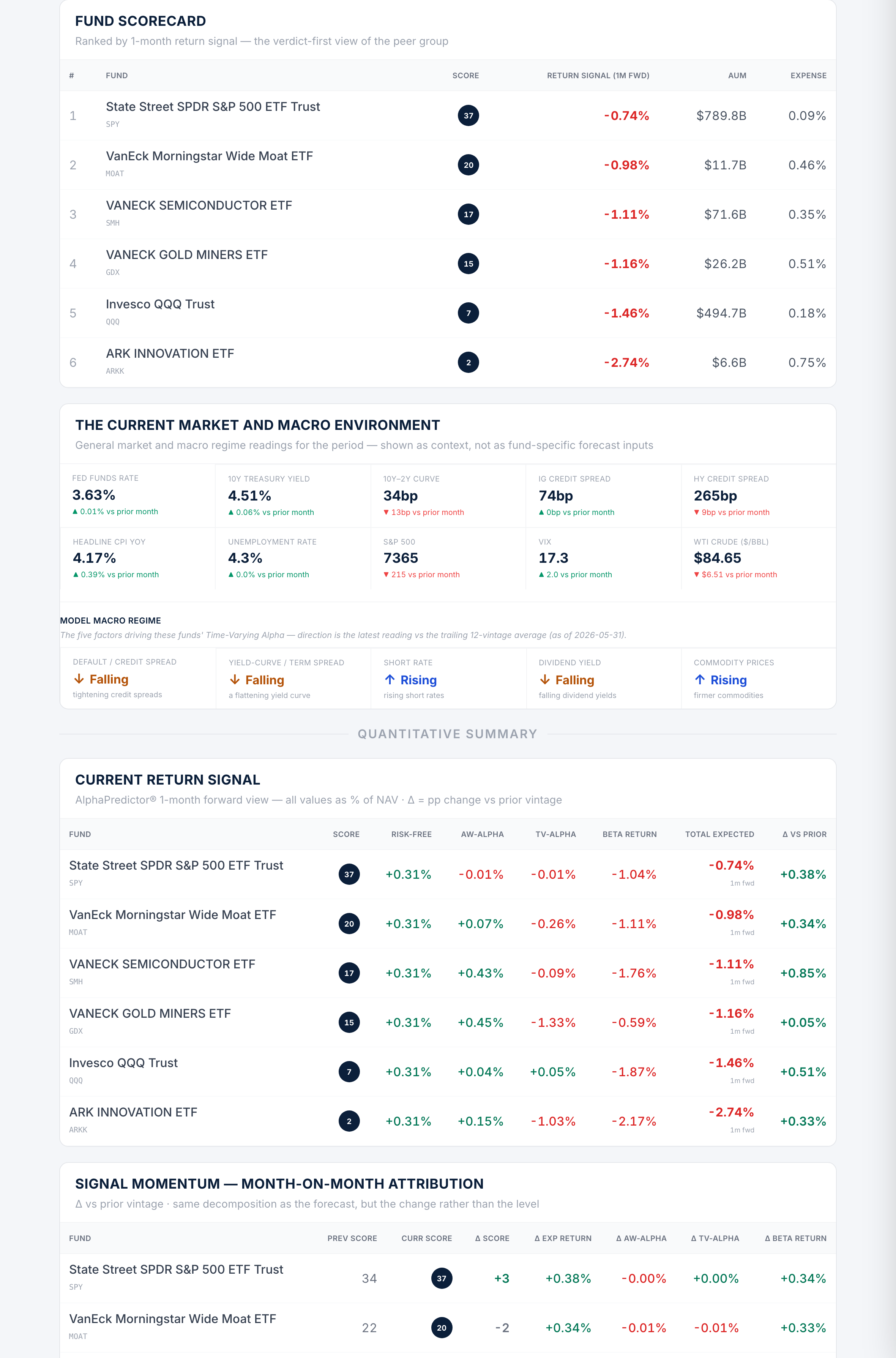

Every ETF's return signal for the coming month is ranked into a percentile against the full universe — 100 = the strongest signal, 0 = the weakest — and broken into the components that drive it: all-weather alpha, time-varying alpha, and factor return. Sort 1,225 funds in one view, or filter to a category and find the strongest names instantly.

- ▸ Return signal decomposed into alpha vs beta, not a black box

- ▸ Factor and macro exposures as z-scores against the whole universe

- ▸ Natural-language screening — "cheapest tech with strong momentum"

Drill into any fund

Every number traceable to the model

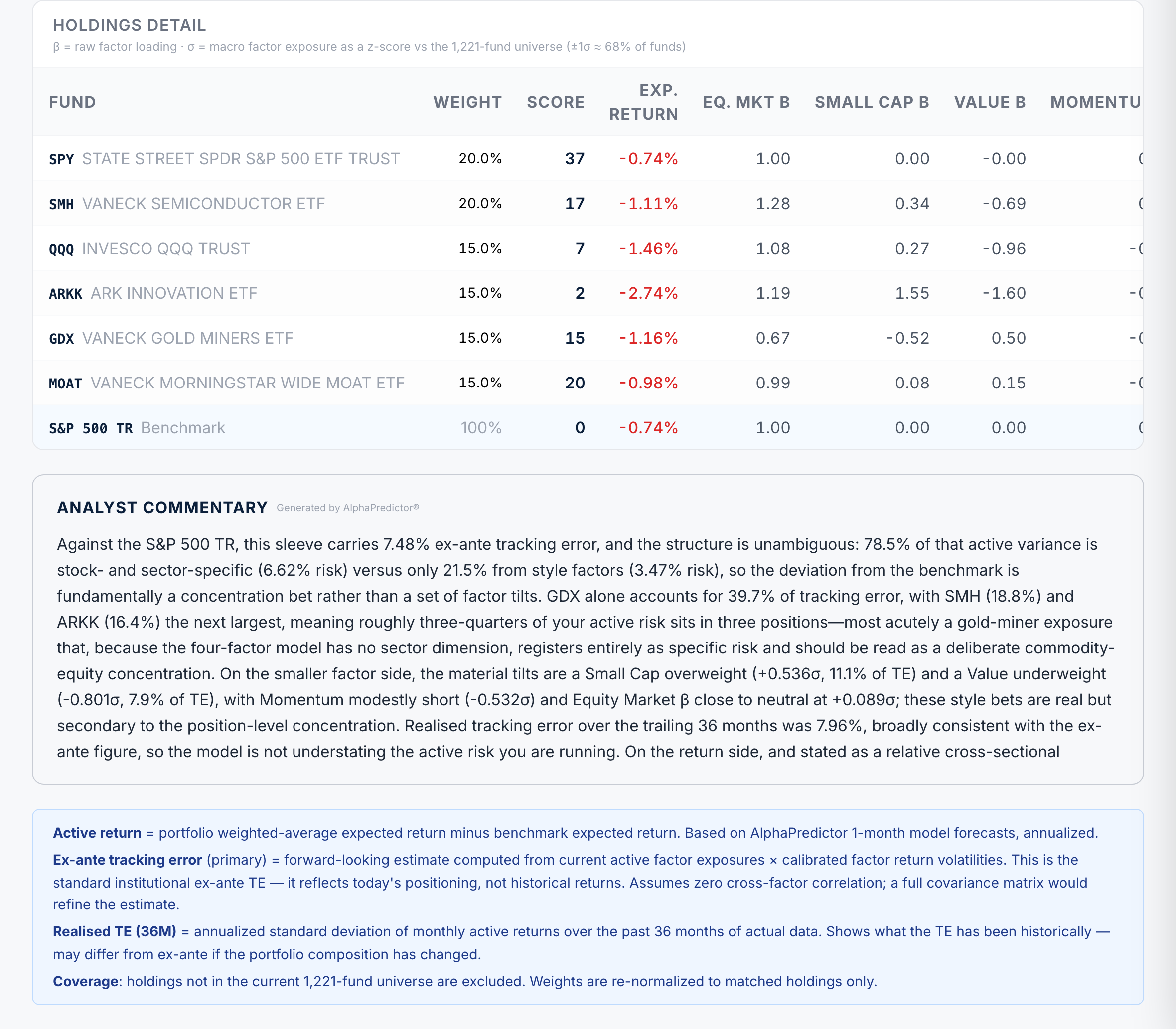

Click a fund and the full picture opens: the return signal broken into all-weather alpha, time-varying alpha, factor return and the risk-free rate — then the factor and macro exposures behind it, each scored against the whole universe. Here, energy's XLE earns a 98 AlphaScore from a positive alpha and value tilt, even as its equity-market beta is a drag this month.

- ▸ Expected-return waterfall: where every basis point comes from

- ▸ Beta and macro sensitivities as ±σ z-scores vs all 1,225 funds

- ▸ Trailing performance, AUM, expense ratio and benchmark in one place

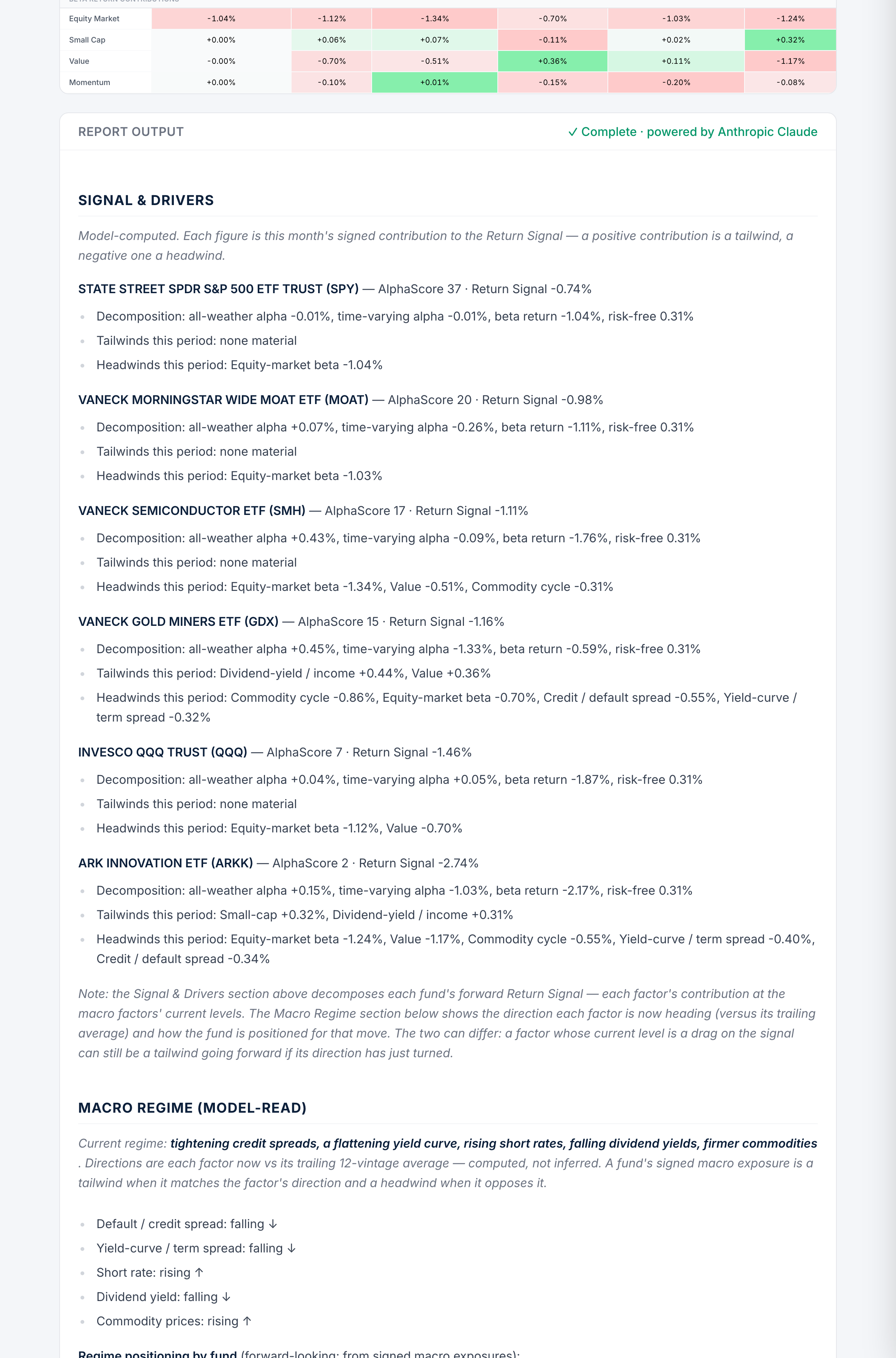

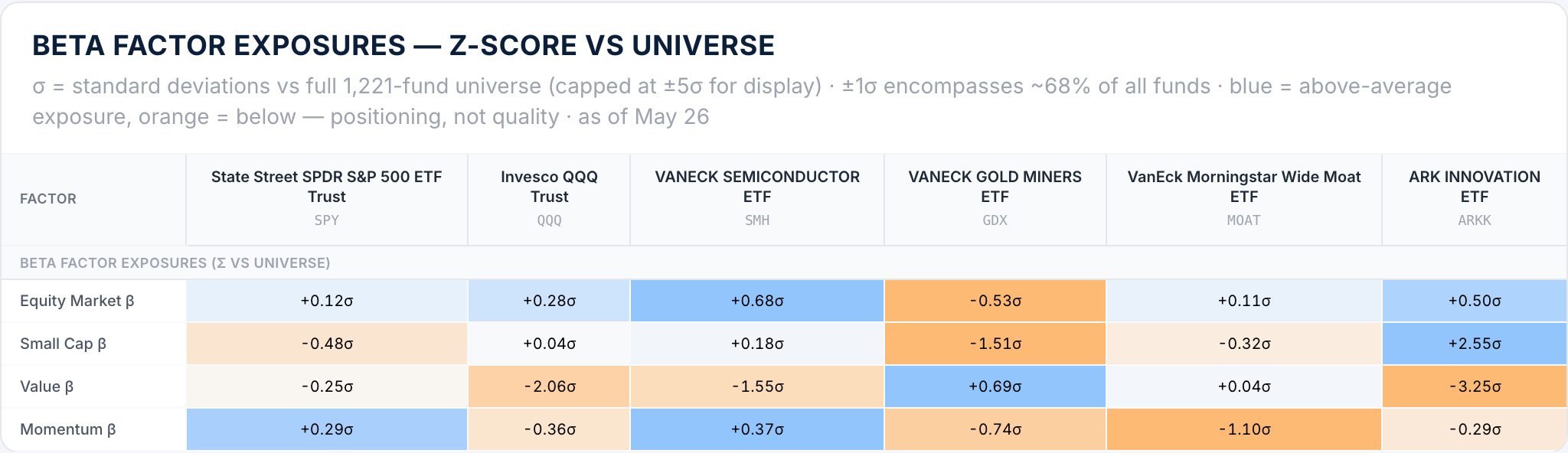

Factor heat maps

Every exposure, mapped against the universe

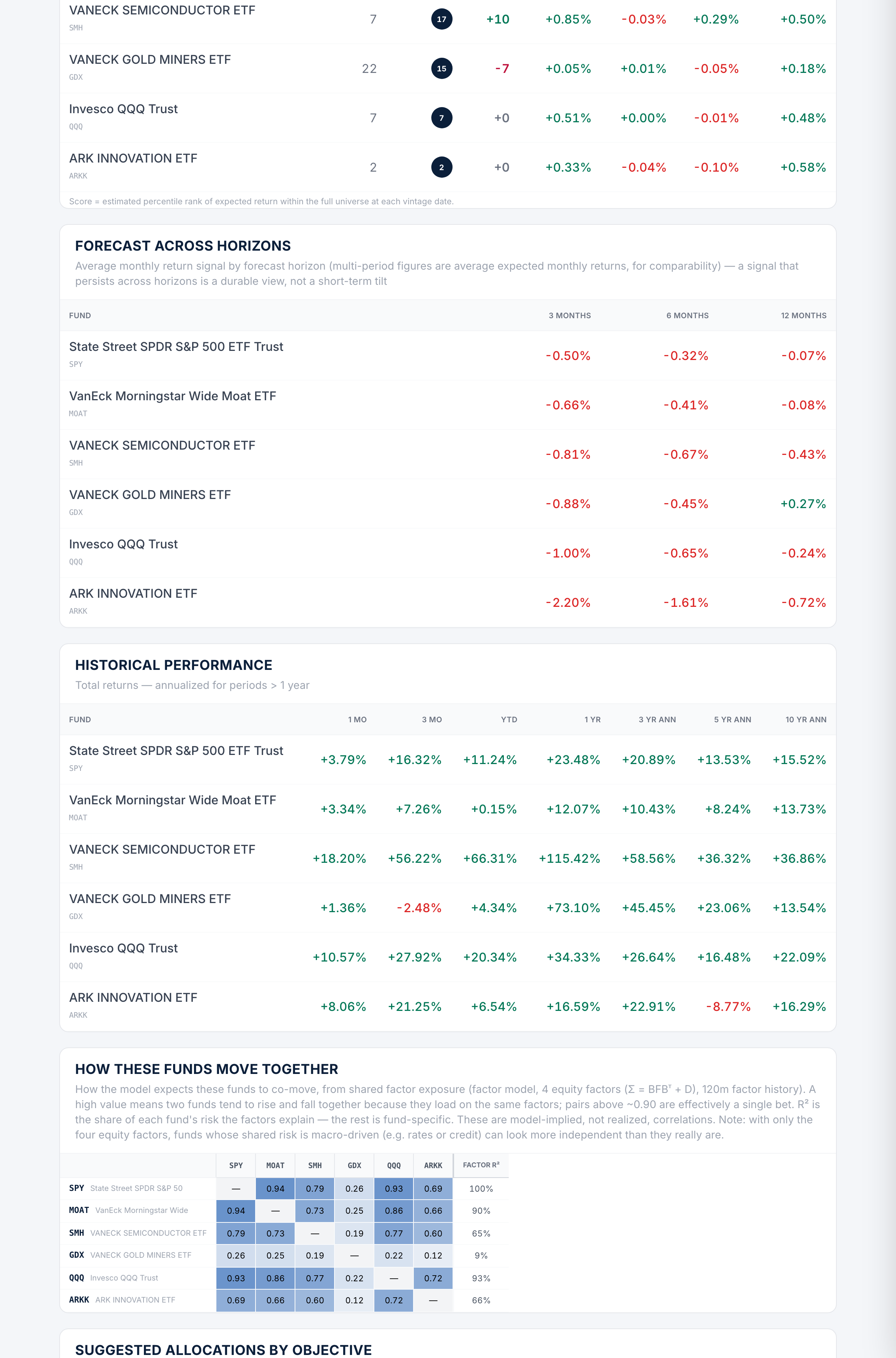

See each fund's tilt to the equity-market, size, value and momentum factors as z-scores against all 1,225 funds. Blue runs above average, orange below, so a peer group's positioning reads in a single glance.

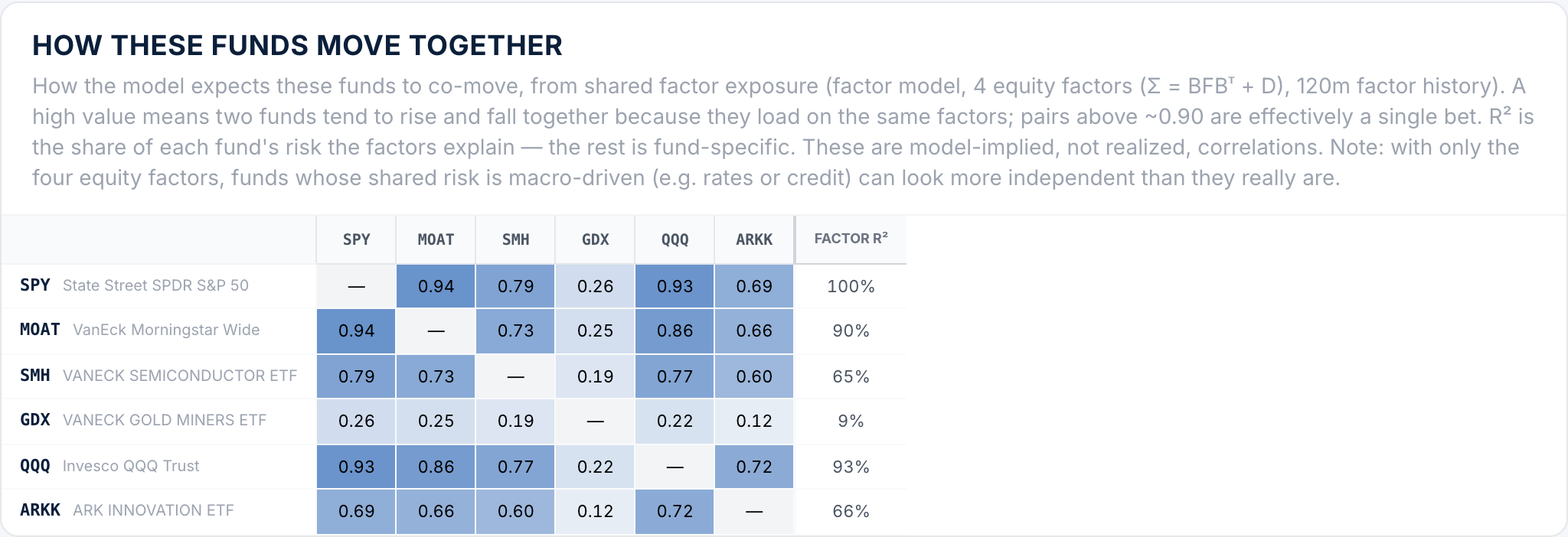

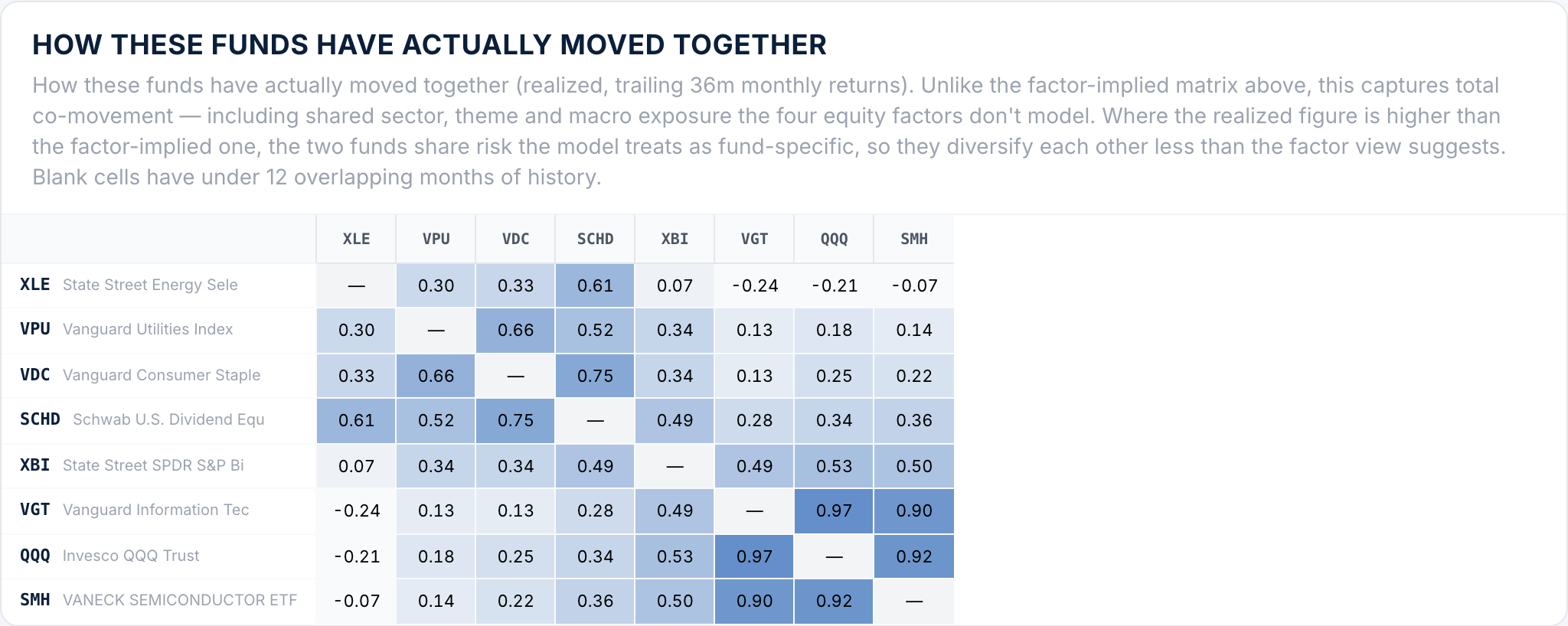

See the overlap

Know how different your funds really are

Two views of co-movement, side by side: what the factor model expects from shared style exposure, and how the funds have actually moved together over the past three years. Where realized correlation runs far above the factor view, two funds share sector or theme risk the style factors don't capture — they diversify each other less than they appear to. It's the co-movement check most screeners can't do.

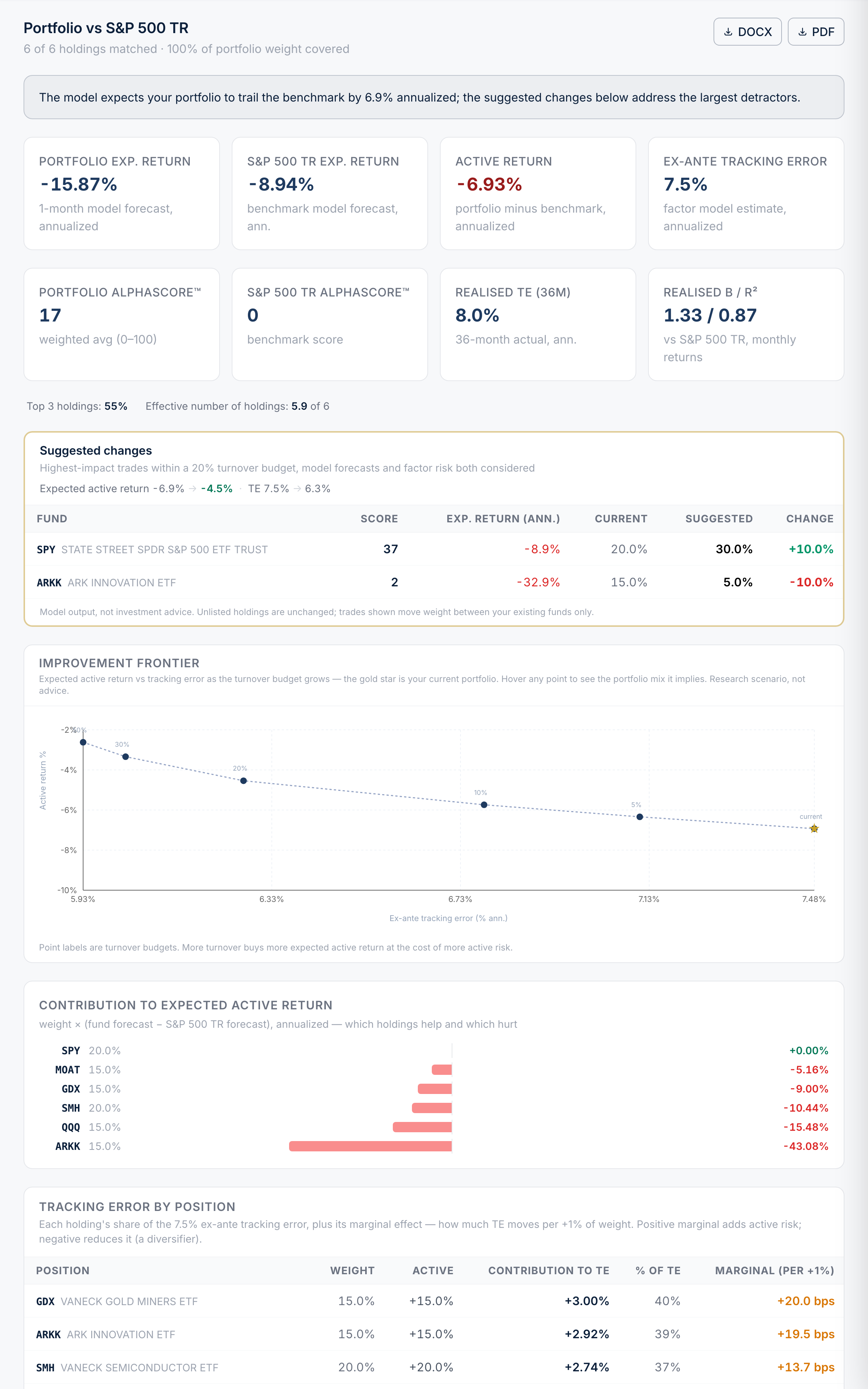

Portfolio analyzer

Build it, stress-test it, see what to change

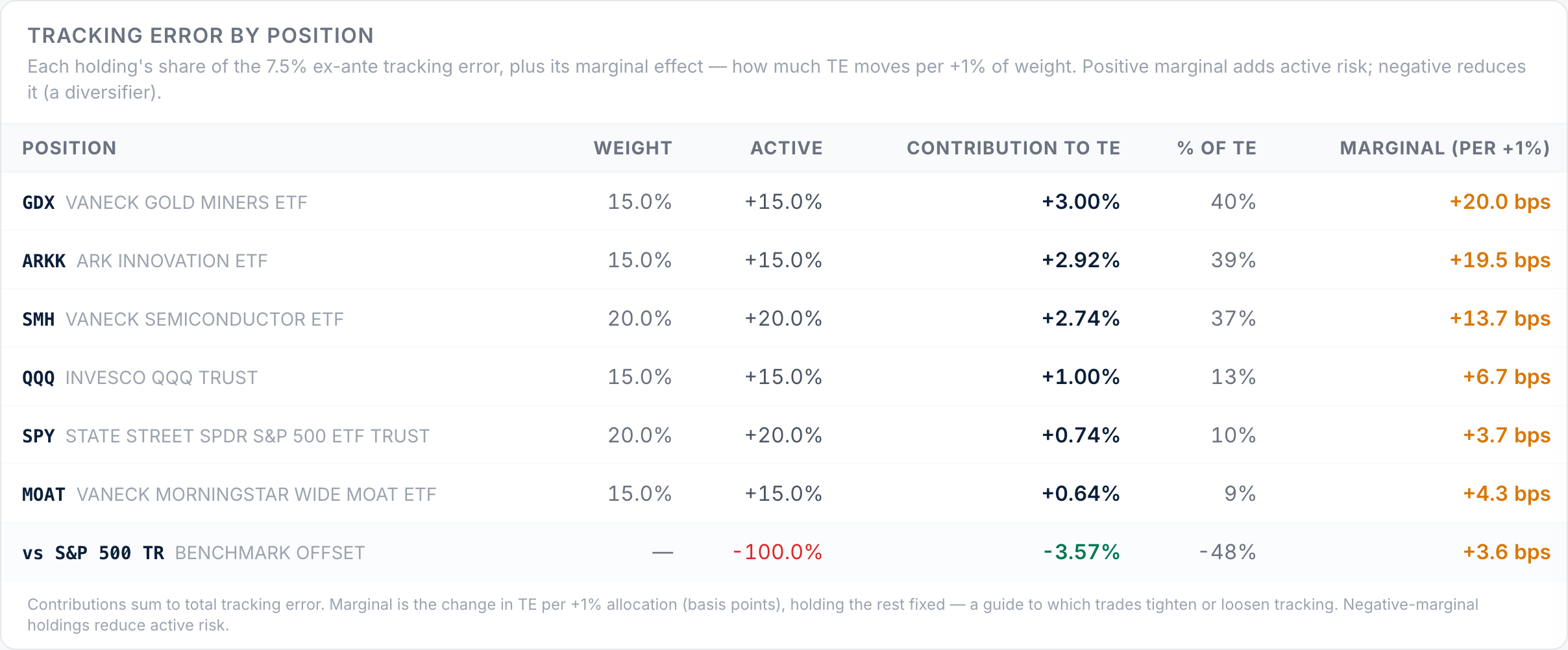

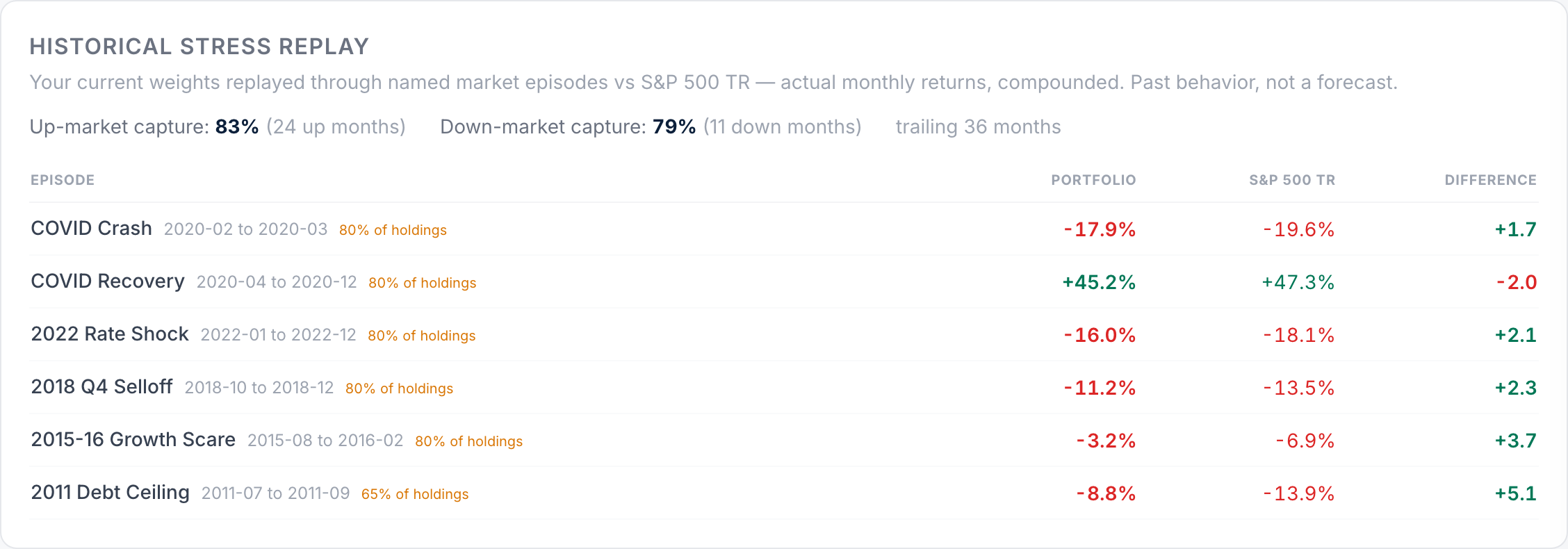

Paste any portfolio and measure it against a benchmark: tracking error decomposed into factor (style) tilts versus stock- and sector-specific concentration, the holdings that drive it, and the model's relative return view. Then replay your exact weights through real market episodes — the COVID crash, the 2022 rate shock, 2018's Q4 — and see up- and down-market capture. Actual history, not a simulation.

- ▸ Tracking error split into factor (style) and stock/sector-specific contributions

- ▸ Named stress episodes plus up/down-market capture — from actual fund returns

- ▸ Suggested trades to tighten or loosen tracking, within a turnover budget

Build → Analyze

Build the portfolio, then take it into the client meeting

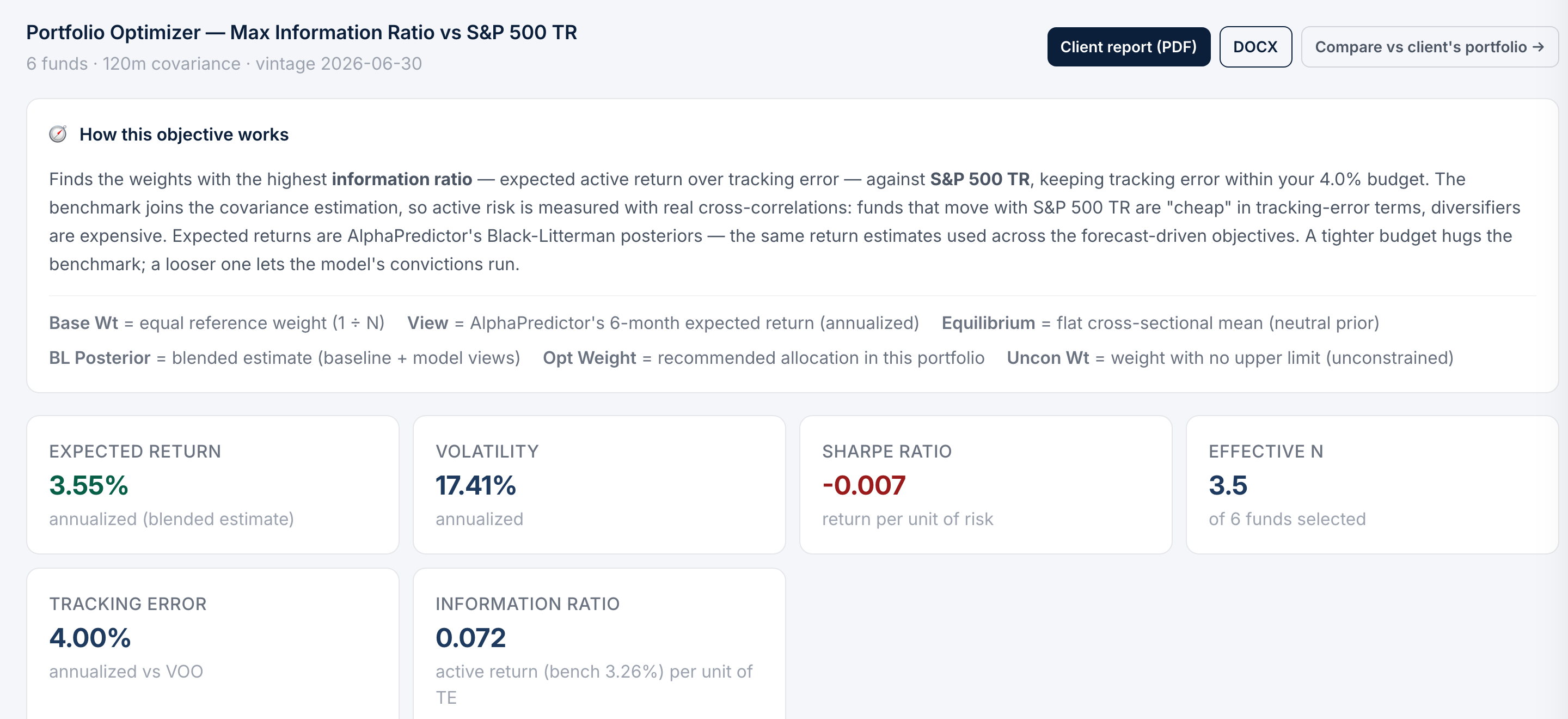

Turn a shortlist into recommended weights with a Black-Litterman engine on AlphaPredictor's 6-month forecasts — maximum information ratio inside a tracking-error budget, or four other objectives. Then export a client-ready construction report on the spot, or put the build next to the client's current book — their portfolio is never touched.

- ▸ Every weight explained: base weight → model view → equilibrium → blended posterior

- ▸ One-click construction report — PDF or Word, written commentary in every export

- ▸ Compare against the client's book without ever overwriting it

Advisor toolkit

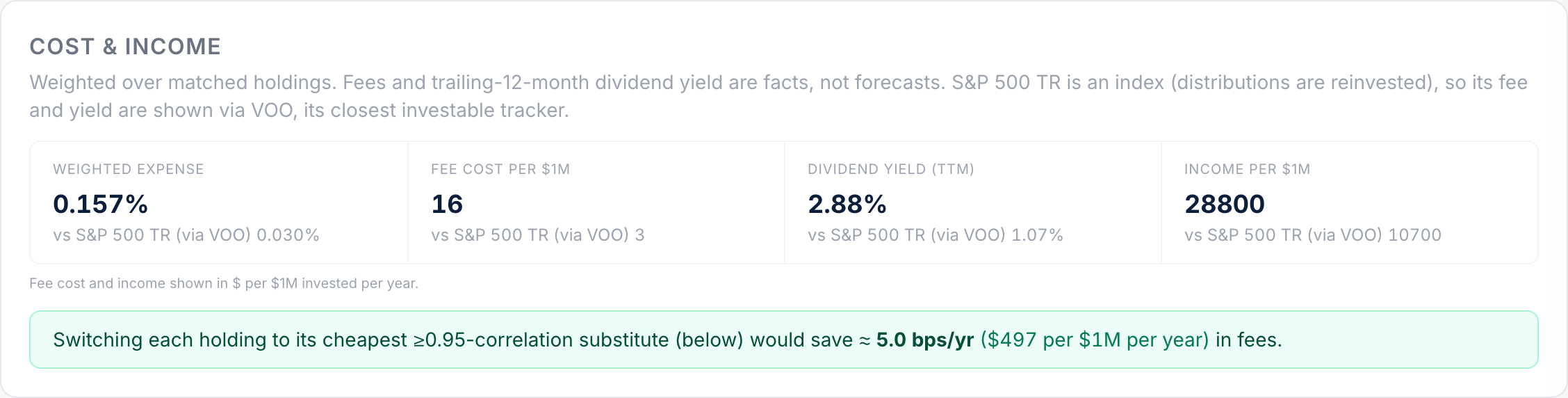

Fees, income and taxes — facts your clients can act on

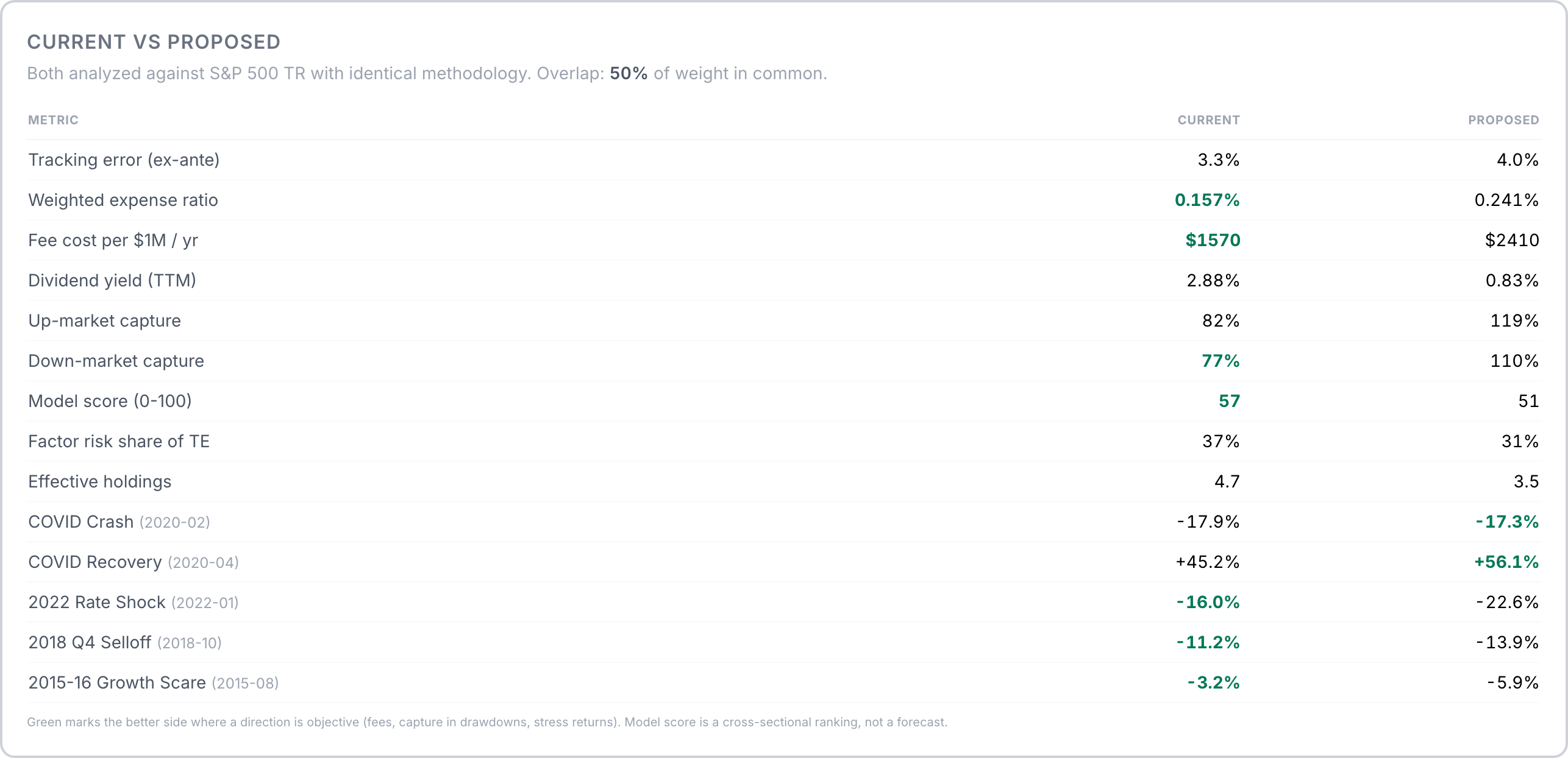

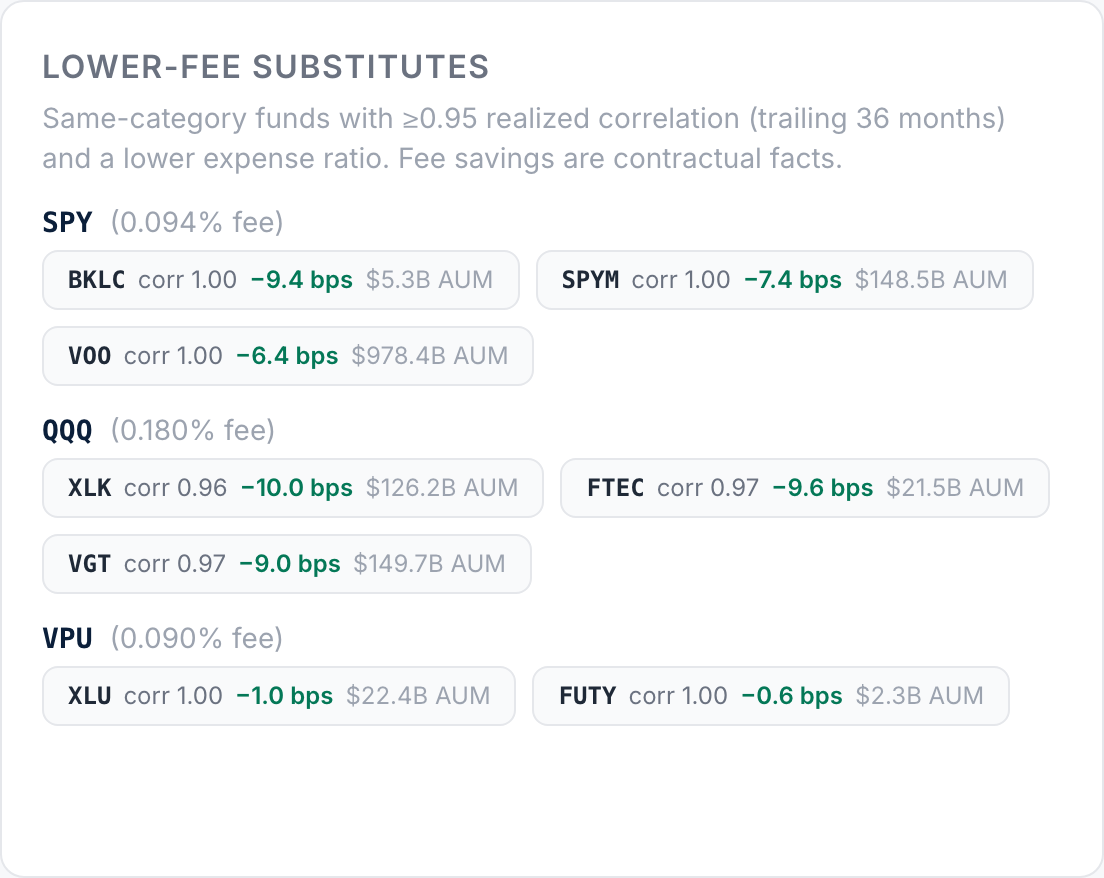

Every number here is contractual or realized — expense ratios, trailing dividends, observed correlations — never a forecast. Find same-exposure funds at a lower fee and wash-sale-conscious tax-loss-harvesting partners, see the portfolio's income in dollars per million — and price any swap with one click: “See impact” re-runs the whole book with the substitute in place, side by side with the current version.

- ▸ White-label the PDF and Word exports with your firm's name and logo

- ▸ A monthly plain-text client update, composed from the model's own numbers

- ▸ Not tax or investment advice — decision support built on verifiable facts

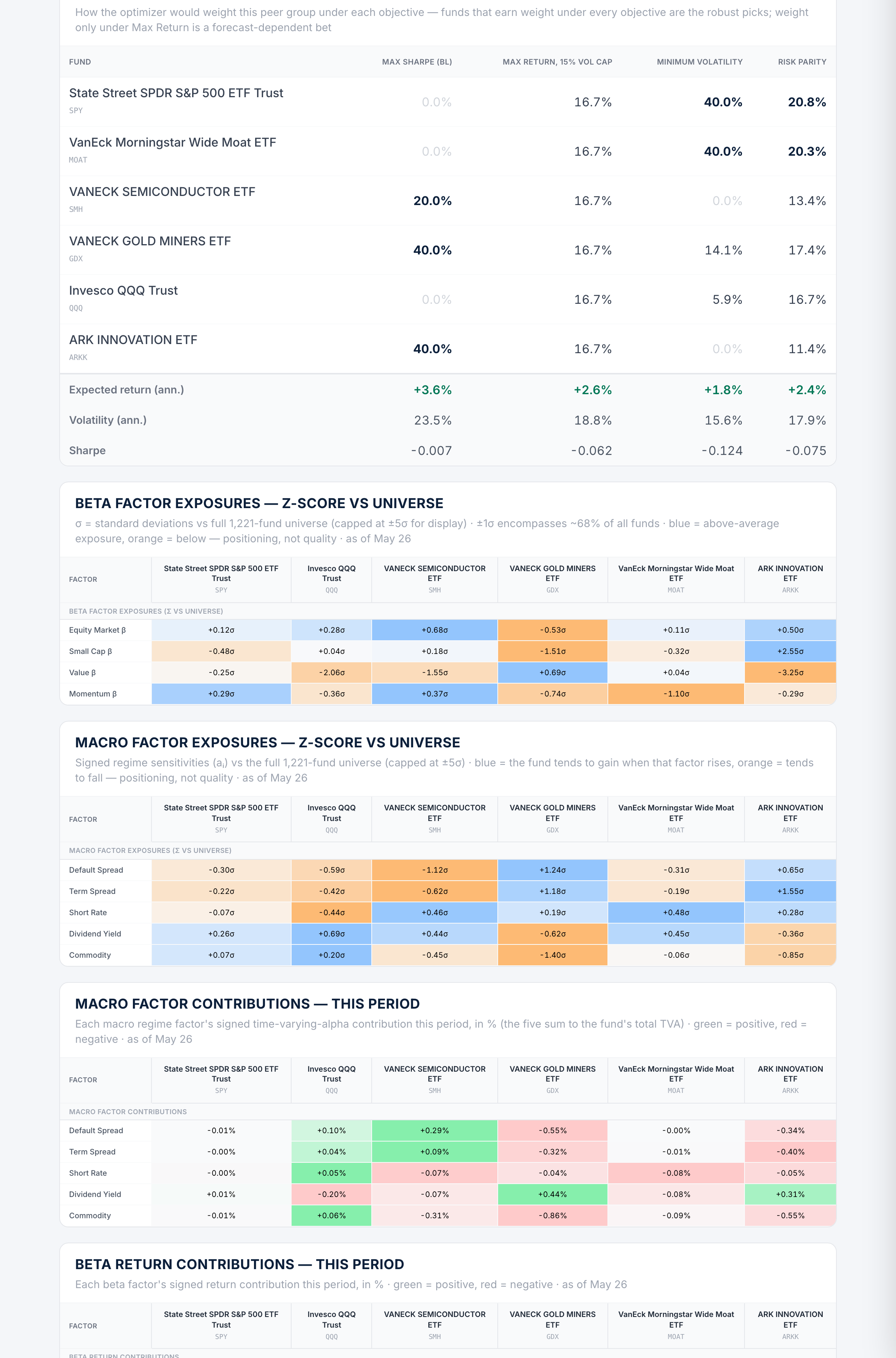

In the Insights report

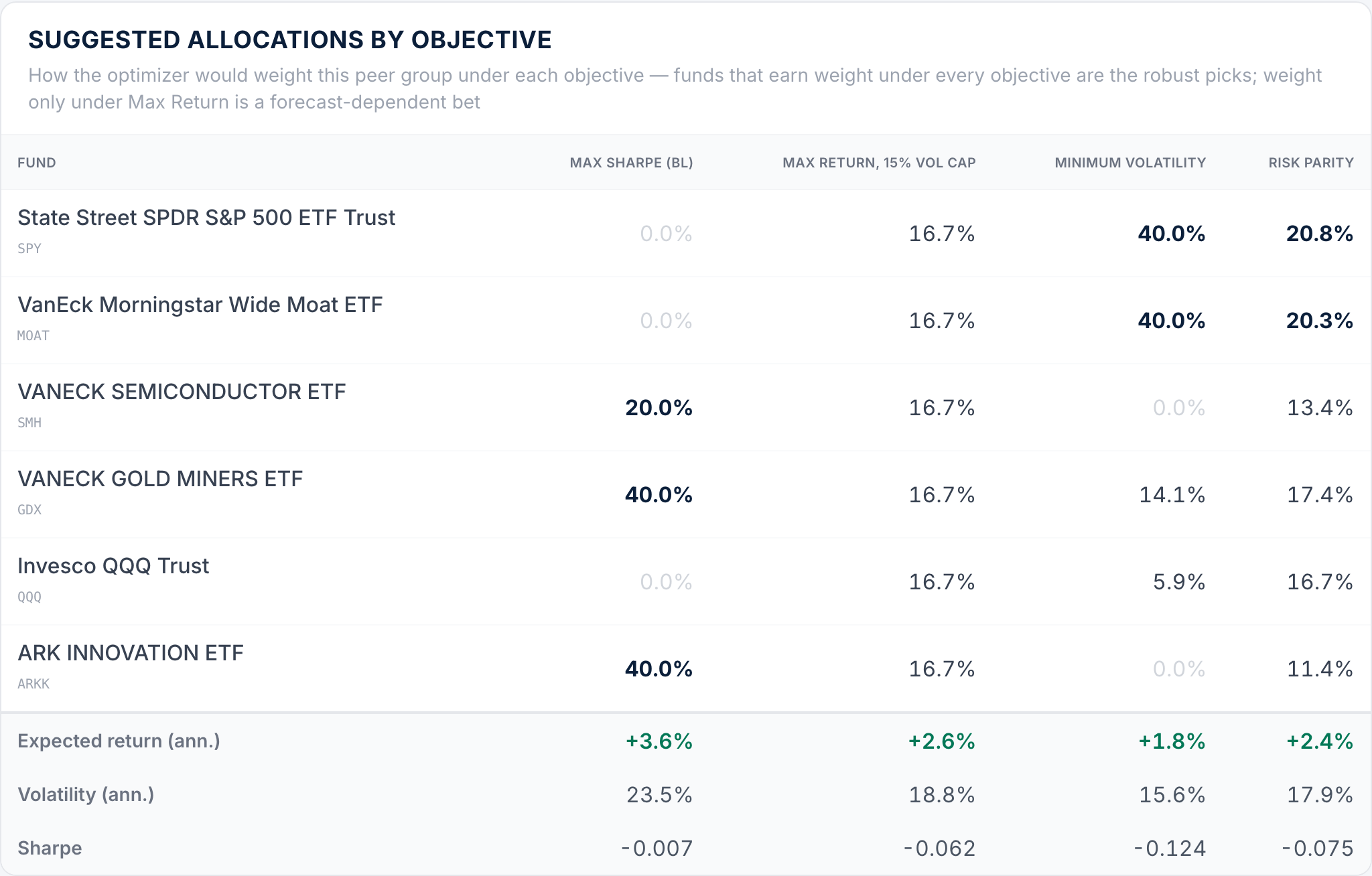

One peer group, four ways to weight it

The Insights report proposes allocations under four objectives at once — max Sharpe, max return within a volatility cap, minimum volatility, and risk parity — over a factor-aware covariance. Funds that earn weight under every objective are the more robust candidates; weight only under max-return signals a forecast-dependent position.